Inflation has been soaring and your money can not buy what it used to, but take heart Americans the IRS has taken notice. In response to high inflation, the IRS has recently adjusted all of the income tax brackets for U.S tax payers to help lower their tax burdens.

Will these adjustments be enough? Will the IRS actually save the day?Today, I’m going to explain what the IRS has changed, and share exactly what all of this means for you.

How Inflation Works

So before we get into the new IRS adjusted tax brackets for 2024, there’s a couple of things you need to know about how inflation works. Once you grasp this, you will better understand how it’s impacting your personal finances, and why the IRS made these changes.

Let’s start off by defining inflation. Inflation is the gradual increase in the cost of goods and services. As prices go up, the purchasing power of your money decreases. In other words, you can’t afford what you used to.

Now, we all know how inflation has risen across the whole United States. But Floridians listen up, inflation is causing food prices to spike faster in Florida than in any other state.

In fact, Florida prices have gone up by 17.5% in the last 4 years, and household products have risen about 24% as well. Between the 2 of them, that averages to about a 20% increase in the cost of goods. That is crazy!

How Inflation Impacts You?

So what does this mean? Just imagine you are going to the grocery store, Walmart, Whole Foods with $100 So you’re about to walk into the store and inflation comes along and takes $20 from you, and that is $20 you will never see again.

Now, what you are left with is just $80 to get what you need. At this point, you might be thinking oh well there goes my Ben & Jerry’s.

But imagine this times 10, imagine this is one thousand dollars and you just lost $200. This is a serious difference. What is it that you won’t be able to get or pay for this month because you just lost that $200?

Meet the New 2024 Tax Bracket Adjustments

So, how does fighting inflation factor into the 2024 tax bracket adjustments?

Well, the way tax brackets work is they are designed so that different income levels or income brackets pay different amounts of Federal taxes. Generally the more money you make, the more you are taxed. Pretty simple and straight forward right.

By adjusting the income levels of the tax brackets, the IRS helps to ensure you are not forced into a higher tax bracket just because you received a raise at work to keep up with inflation.

Now, let’s look at the 2024 adjustments for the most common tax brackets to see which one you fall into.

The 10% Tax Bracket

So if you are single in 2024 and you make $11,600 or less, you belong to the 10% tax bracket. For married couples, they can make up to $29,200 to belong to the 10% tax bracket.

And in 2023, the single filers can earn up to $11,000 or less and married couples $27,700 to belong to the 10%, so the IRS has increased the tax brackets to accommodate inflation.

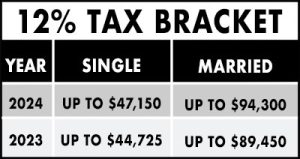

The 12% Tax Bracket

Now, let’s talk about the 12% tax brackets for 2024. If you are single in 2024, you can make up to $47,150 and married couples can earn up to $94,300.

And in 2023 for the 12% tax bracket, single filers can make up to $44,725 and married couples combine their salaries up to $89,450.

The 22% Tax Bracket

Now for the 22% tax brackets, if you are single in 2024, you can make up to $100,525 and for married couples $201,050 or less to belong to the 22% tax bracket

The 24% Tax Bracket

Now, one last bracket I would like to talk about is the 24% tax bracket. As a single filer, you can make up to $191,500 and married couples $383,900 in 2024.

But wait, there’s more!

2024 Standard Deduction Changes

The IRS has made more key changes for 2024 that is designed to help besides adjusting the income tax brackets. For 2024 the IRS has also increased the standard deduction for 2024 to help your dollar go further.

For those that don’t know what this is, the standard deduction is a fixed dollar tax deduction set by the IRS that reduces your taxable income and is claimed by most Americans each year.

Now, I’ll show you how it works, and how it effects you and your income as single and married couples.

So in the first filing status, it’ll be a single person that we’ll assume has the income of $95,379, in 2023. With the standard deduction of $13,850, you would have paid in taxes $13,243.

Now in 2024 the standard deduction will be $14,600, so your taxes for 2024 will be $12,823, that is a $420 savings when compared to 2023.

Now what if you’re not single, you’re married, how does that work?

Normally, the tax tables favor married couples. So in 2023, if you you are married making $95,379, you would have paid $7,681 in taxes. Now in 2024, you would pay $7,477 because the standard deduction increased to $29,200, and that gives you savings of $204 compared to 2023.

Get Your Appointment Today!

If you don’t already know me, my name’s Sonia Narvaez. I’m a licensed CPA and wealth building strategist with over 25 years experience.

And if you have any questions about how to take advantage of any of these tax savings strategies, book your tax estimate with a member of my team, simply click this scheduling link, and pick the time that works best for you.

We would love to help and meet with you.