Short answer? Yes, you should buy a home in 202, but not for the reasons most people think.

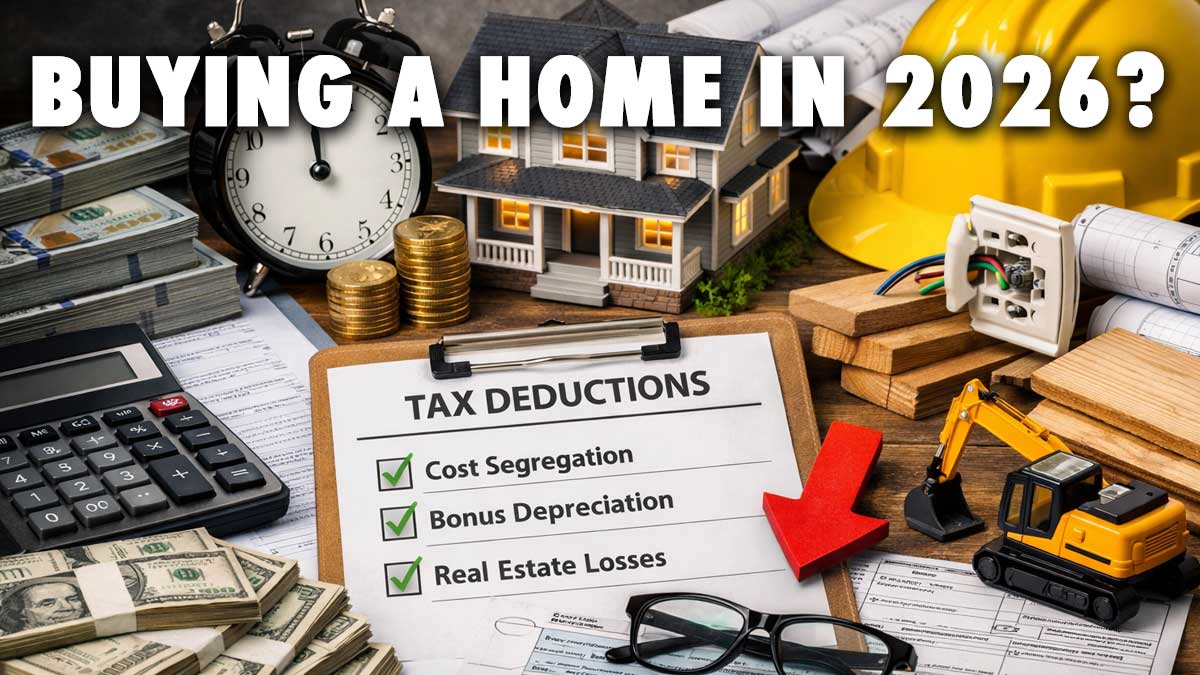

Real estate is still worth it in 2026 because of powerful tax strategies like cost segregation, bonus depreciation, and real estate losses.

Let’s break this down in plain English… no accountant jargon, no eye-glazing nonsense.

What Is Cost Segregation (And Why Should You Care)?

Cost segregation sounds complicated, but it’s really just a fancy way of saying:

“Break your property into parts so you can write things off faster.”

Here’s how it works:

Let’s say you buy a house for $600,000.

- You don’t depreciate land (so let’s subtract $200,000)

- That leaves $400,000 to depreciate

- Normally, that gets spread over 27.5–29 years

That gives you roughly $13,500/year in depreciation.

But here’s where things get interesting…

With a cost segregation study, you break the property into components:

- Flooring → depreciated over 5–7 years

- Cabinetry → shorter lifespan

- Electrical systems → faster write-offs

Now instead of spreading everything out slowly, you accelerate depreciation.

Result?

Higher write-offs → Lower taxable income → More money in your pocket.

Bonus Depreciation: The Real Game Changer

Now, this is where things get really spicy.

Bonus depreciation allows you to write off a massive portion—or sometimes all—of certain assets upfront.

And in recent times, Bonus Depreciation is back in a big way.

For Example:

Let’s say you invest in a $250,000 movable property (like a “box house” or mobile structure).

- This can qualify as equipment

- You may be able to write off 100% of it immediately

Now watch this:

Let’s assume you earn $250,000 in W2 income, but you invested in a “box house” property.

Your taxable income could drop to $0.

Yeah. Zero.

That’s not a loophole, it’s a very smart strategy.

But Wait… Can You Do This With Regular Real Estate?

Not exactly.

You can’t write off the entire property unless it qualifies (like movable assets).

But…

With cost segregation + bonus depreciation:

- You can write off things like flooring, cabinets, fixtures

- You can accelerate those deductions

- You can significantly reduce your taxable income

So while you may not wipe out everything instantly, you can still make a huge dent in your tax bill.

Using Real Estate Losses (Yes, It’s Still Allowed)

Now let’s talk losses… because oddly enough, losses can be a good thing.

Here’s the deal:

- If you earn under $100,000

- You can write off up to $25,000 in rental losses

That directly reduces your taxable income.

But it gets better for certain people such as:

- Short-term rental owners

- Active investors

- Real estate professionals

These groups can often bypass limitations and unlock even bigger tax benefits.

Translation: The more strategic you are, the more money you keep in your pocket. This is why it pays to be proactive!

Real Example: What This Actually Saves You

Let’s say bonus depreciation gives you a $70,000 write-off.

If you’re in a 20% tax bracket:

You just saved $14,000 in taxes.

Not by working more… not by cutting expenses…

Just by structuring your investment smarter.

So… Is Real Estate Still Worth It in 2026?

Absolutely.

You’re getting:

- Cash flow

- Appreciation

- Tax advantages

That’s a pretty unfair combo.

Yes—it takes effort. Yes—it requires upfront money.

But compare that to trading 40+ hours a week for income…

It’s not even the same game. Let that sink in. The game is completely different.

Final Thought

Real estate in 2026 isn’t just about buying property.

It’s about playing the tax game correctly.

And if you do?

You don’t just make money… you keep more of it.